Responding the the Financial Crisis

Monthly Purchase Made in $billions

As a result of the subprime mortgage crisis, the financial system underwent a period of severe tumult, beginning in late 2008. A myriad of banks were either failing or under extreme stress as their assets, like mortgage-backed securities (bonds backed by mortgage payments), plummeted in value, credit markets froze and the economy contracted. In response, the Federal Reserve pursued expansionary monetary policy and increased the money supply in order to avoid a deflationary spiral of increasing unemployment, lower production, lower wages, lower demand, and lower prices. Put simply, they were trying to avoid another Great Depression. Therefore, the Federal Reserve purused numerous policies and programs to provide credit to the system during the crisis in order to stabilize the market and combat this downward spiral.

In a dramatic attempt to lower the cost of borrowing, interest rates were quickly lowered close to 0%, an act never before seen--but a traditional move by the Federal Reserve nonetheless. Additionally, numerous liquidity facilities were created by the Federal Reserve as more traditional facilities and operations proved inadequate in alleviating the ills of the financial sytem. Both of these acts were done in the hopes that cheap and readily available credit would maintain liquidity, stabilize the credit market and prevent further economic contraction.

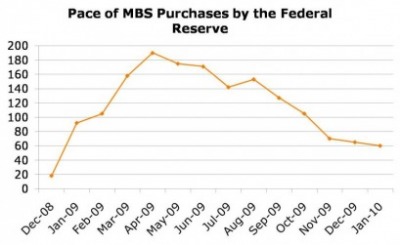

Furthermore, the Federal Reserve purchased mortgage-backed securities (MBS), from various financial institutions en masse, as shown in the graph above. This was done in order to remove those "toxic assets" from banks' balance sheets in order to prevent further financial losses and more bank failures. In total, the Federal Reserve purchased $300 billion of Treasury securities, $1.25 trillion of agency MBS (those issued by government sponsored enterprises, like Fannie Mae) and about $175 billion of agency debt. These purchases, along with the purchase of private label MBS (those issued by private firms) and the creation of the liquidity facilities, increased the Fed's balance sheet by $2.2 trillion. The Federal Reserve's purchases have had the effect of leaving the banking system highly liquid, with U.S. banks now holding more than $1.1 trillion of reserves with Federal Reserve Banks. Most of these reserves were intended to back up loans, but instead they have piled up as the lending activity of banks declined.

Most of these programs seem to have achieved the desired overall effect; the financial market has stabilized (as has the stock market), banks are profitable again and the economy is beginning to grow. However, the size and scope of the invovement of the Federal Reserve in the financial system is sustainable only as long as the economy is frail, and output and consumption is weak. With the ongoing economic recovery, the exit strategy of the Federal Reserve with regard to these policies will be exceedingly important.