Recovering from the DotCom Bubble

In response to the burst of the DotCom bubble in 2001 and the terrorist attacks on 9/11, Greenspan lowered the federal funds rate, the interest rate banks charge eachother for loans, by 4%, bringing it to 6.5%. It was lowered again in 2003 bringing it to an all time low of 1%. Lowering the federal funds rate makes it cheaper to borrow, which promotes economic growth as lending increases.

Greenspan wanted to encourage homeownership and make it easier for people to own homes. With this in mind, various exotic loans were introduced: subprime mortgages, loans to individuals who would otherwise not qualify for stantard home loans because of bad credit history, and adjustable rate mortgages(ARMs), where the borrowers initial payments are low and there is not a fixed rate therefore after two or three years, the interest payments can pop up. Though these loans were very risky, people who once could not own homes now could.

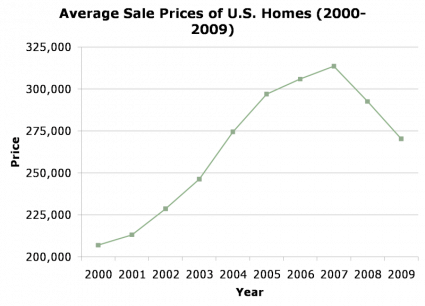

In the first graph, we see the average sales prices of US homes steadily increasing since 2000, after the burst of the DotCom bubble. It peaks in 2007, prior to the housing bubble bursting and has since been on the decline.

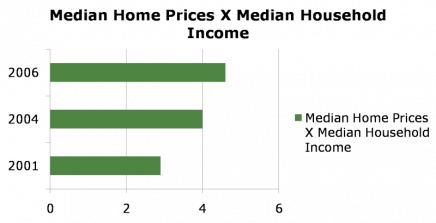

Because the average home prices became so large in relation to household income, as seen in the second graph, people began refinancing, taking out second mortgages. Those with ARMs could not refinance to avoid the higher payments and began to default. From 2006-2007 the US saw a 79% increase in foreclosures.

Greenspan wanted to encourage homeownership and make it easier for people to own homes. With this in mind, various exotic loans were introduced: subprime mortgages, loans to individuals who would otherwise not qualify for stantard home loans because of bad credit history, and adjustable rate mortgages(ARMs), where the borrowers initial payments are low and there is not a fixed rate therefore after two or three years, the interest payments can pop up. Though these loans were very risky, people who once could not own homes now could.

In the first graph, we see the average sales prices of US homes steadily increasing since 2000, after the burst of the DotCom bubble. It peaks in 2007, prior to the housing bubble bursting and has since been on the decline.

Because the average home prices became so large in relation to household income, as seen in the second graph, people began refinancing, taking out second mortgages. Those with ARMs could not refinance to avoid the higher payments and began to default. From 2006-2007 the US saw a 79% increase in foreclosures.

Back to Greenspan Era